In times of uncertainty, inflation and rising costs of living, financial literacy is becoming a crucial life skill. In this short guide, we will present 5 simple but effective steps to take control over your finances – regardless of the amount of income.

Step 1: Know your financial picture

- Write down all income and expenses.

- Distinguish between fixed costs (rent, electricity) and variable costs (food, leisure).

- Use free apps (e.g. Toshl, EveryDollar) or a simple Excel spreadsheet.

Hint: Review your last 3 bank statements – you'll be surprised how much can drain away "little by little".

Step 2: Set a realistic budget

- Plan your monthly expenses according to the 50/30/20 system:

- 50% urgent expenses

- 30% desire

- 20% savings/long-term goals

- Include an emergency fund (at least €500–1,000) so that you don't get thrown off track by any unforeseen expense.

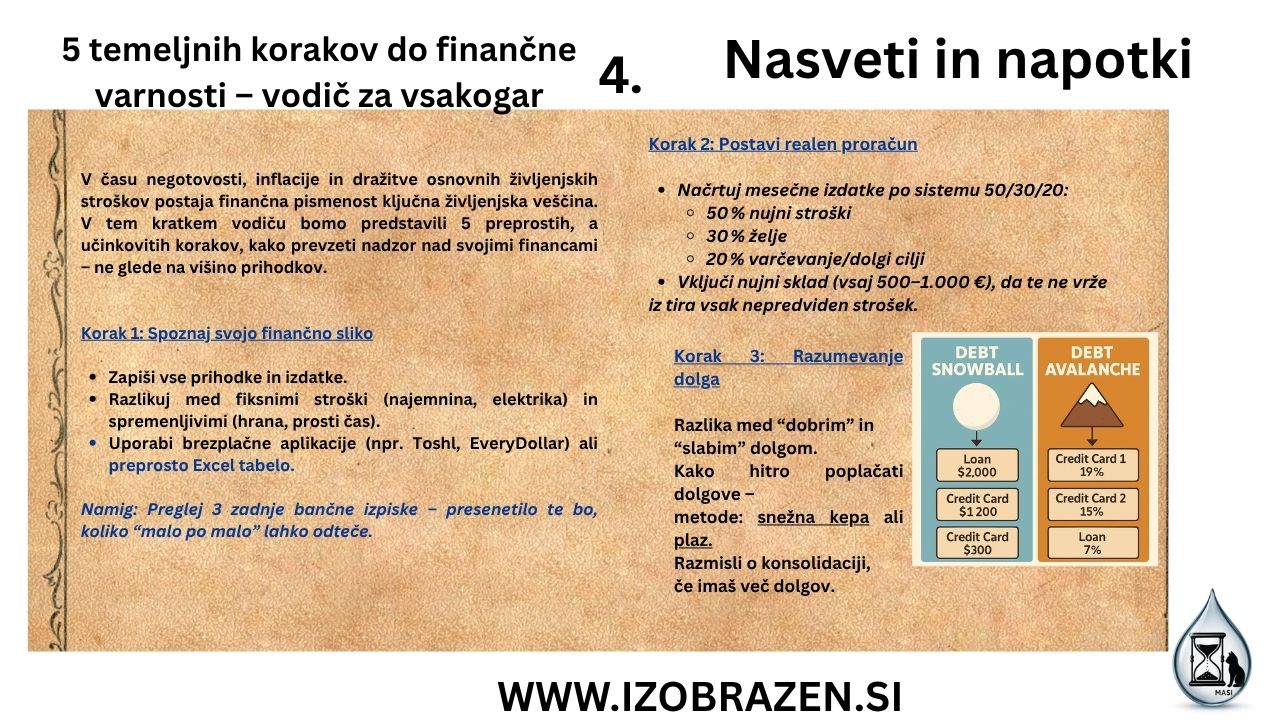

Step 3: Understanding debt

The difference between “good” and “bad” debt.

How to pay off debts quickly – methods: snowball or avalanche.

Consider consolidation if you have multiple debts.

Debt Snowball Method

How it works:

Make a list of all your debts – from smallest to largest, regardless of interest rate.

You pay minimum payments on all debts except the smallest one, which you pay off with any extra money you have.

Once the smallest debt is paid off, you transfer that amount to the next smallest debt – and so on.

Advantages:

- Quick “winning” feelings – you see progress right from the start.

- Increases motivation.

- Psychologically effective because it gives you a sense of control.

Disadvantages:

- You may pay more interest because you don't take interest rates into account.

Debt Snowball Method

How it works:

- Make a list of all your debts – from smallest to largest, regardless of interest rate.

- You pay minimum payments on all debts except the smallest one, which you pay off with any extra money you have.

- Once the smallest debt is paid off, you transfer that amount to the next smallest debt – and so on.

Advantages:

- Quick “winning” feelings – you see progress right from the start.

- Increases motivation.

- Psychologically effective because it gives you a sense of control.

Disadvantages:

- You may pay more interest because you don't take interest rates into account.

Step 4: Saving and investing

- Short-term savings: vacations, household appliances.

- Long-term savings/investment: pension, children, own home.

- Investing basics: stocks, funds, crypto - no illusions about quick profits!

Step 5: Financial goals and routine

- Set clear goals (SMART): “In 6 months I will save €600 for a vacation.”

- 15 minutes every week for finances – checking, planning, adjusting.

- Include your family – especially children – in the conversation about money.

Financial literacy It's not just for the rich or accountants - it's for all of us. Once you understand the basics, you gain the power, freedom, and peace that money can't buy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}